The United States faces simultaneous pressure on housing affordability and food assistance as the nation navigates a prolonged government shutdown. President Trump’s administration confirmed on November 9, 2025, that it is working on 50-year mortgage terms, while the Supreme Court has temporarily allowed withholding of federal food stamp payments affecting 42 million Americans.

Federal Housing Finance Agency Director Bill Pulte confirmed that “we are indeed working on The 50-year Mortgage – a complete game changer.” The proposal emerged as housing affordability reached crisis levels, with first-time homebuyers averaging 40 years of age—the highest on record—and median households spending approximately 38–39 percent of income on mortgage payments.

Simultaneously, the ongoing shutdown created confusion around SNAP (Supplemental Nutrition Assistance Program) payments, with the Supreme Court’s administrative stay on November 8 temporarily permitting the administration to withhold approximately $4 billion in November benefits.

Housing Affordability Reaches Critical Threshold

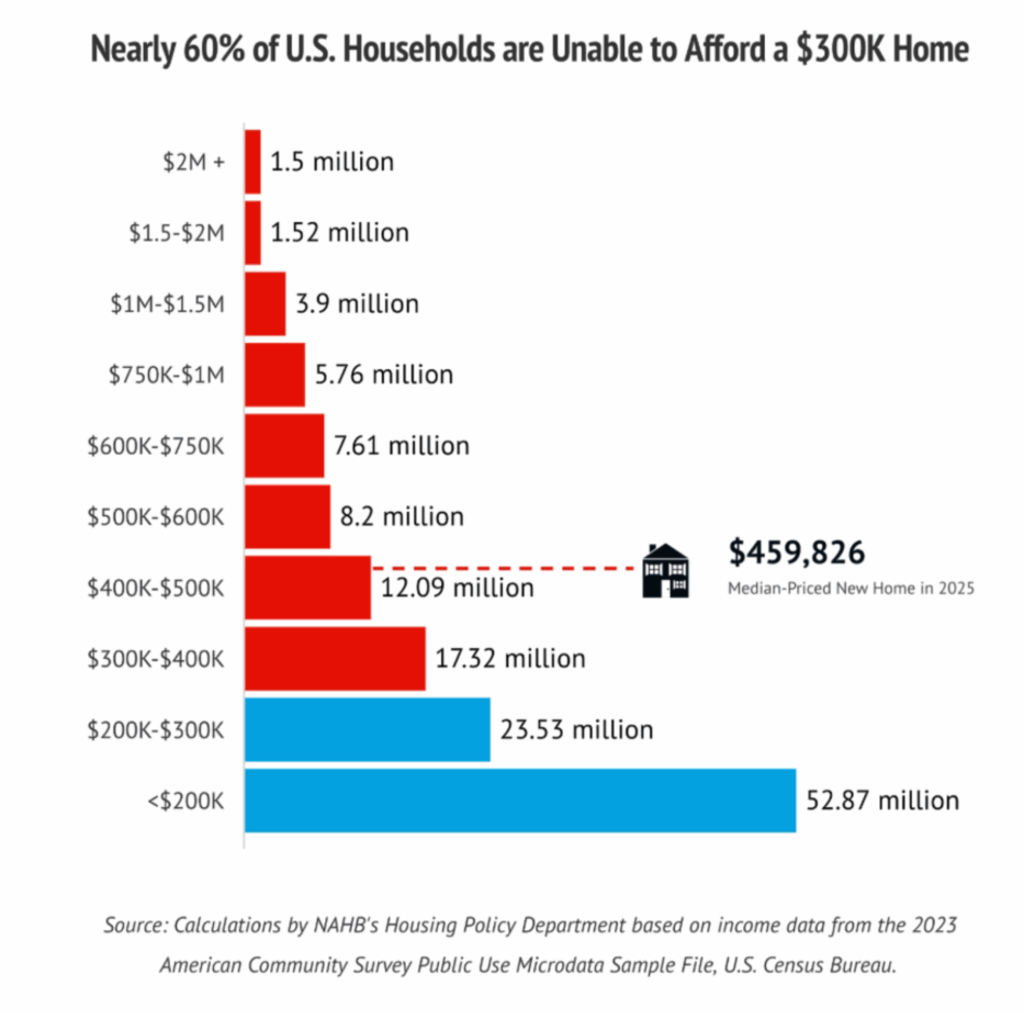

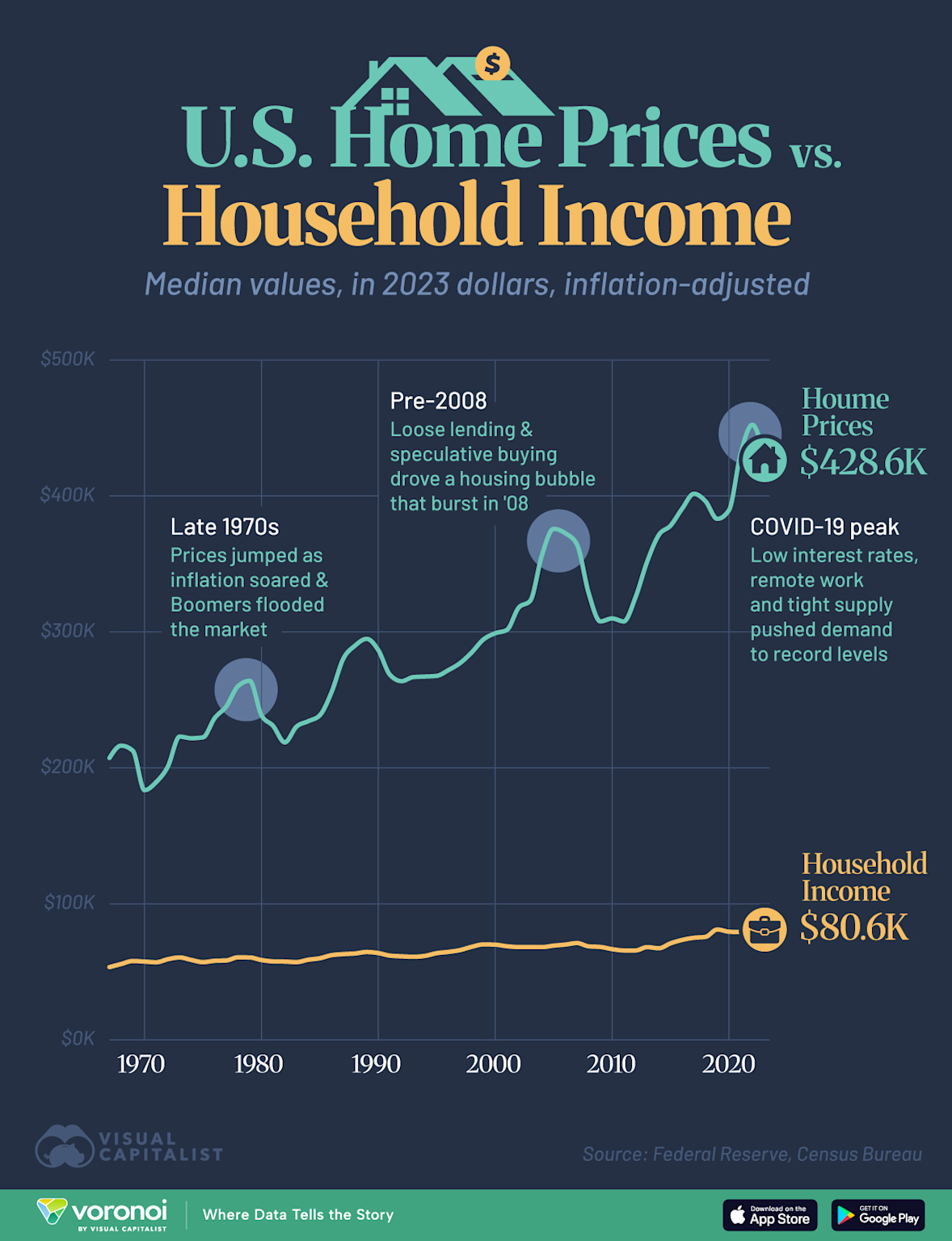

Housing affordability deteriorated sharply during 2025. According to Redfin market analysis, homebuyers currently spend approximately 38–39 percent of monthly income on mortgage payments—well above the historical benchmark of 28 percent. For context, mortgage rates for 30-year loans averaged 6.25 percent as of early November 2025, having remained stubbornly above 6 percent for the majority of the year.

The Mortgage Bankers Association reported that adjustable-rate mortgages (ARMs) comprise approximately 10 percent of all mortgage applications—the highest share in nearly two years. This shift reflects desperation among borrowers seeking lower initial rates despite future payment uncertainty. See also related analysis on Federal Reserve interest rate impacts.

Why this matters: When buyers spend more than 28 percent of income on housing, financial stress increases. At 38–39 percent, households must reduce spending on healthcare, education, and retirement savings. This creates long-term economic pressure across generational wealth-building.

The 50-Year Mortgage Proposal Explained

On November 7, 2025, President Trump shared a social media graphic comparing himself to President Franklin D. Roosevelt, implicitly referencing FDR’s role in standardizing the 30-year mortgage during the New Deal era. Bill Pulte’s announcement on Saturday formalized the administration’s intention to implement 50-year terms.

The mathematics: On a $400,000 loan at 6.5 percent interest:

30-Year Mortgage (Current Standard)

50-Year Mortgage (Proposed)

The tradeoff: The 50-year term reduces monthly payments by $292 but increases total interest costs by approximately $399,280—nearly doubling the interest expense compared to a 30-year mortgage on the same principal. For a 40-year-old first-time buyer, this structure would create mortgage obligations extending to age 90.

Consideration from analysts: Extending debt decades beyond typical earning years raises questions about long-term household financial security and multi-generational wealth accumulation.

SNAP Benefits Freeze: Government Shutdown Impact

When Congress failed to approve funding past September 30, 2025, the federal government shutdown froze SNAP (food stamp) payments beginning November 1. This marked the first time in the program’s 60-year history that benefits ceased entirely at the beginning of a month. For additional political context on budget disputes.

On November 8, the Supreme Court issued an administrative stay permitting the Trump administration to temporarily withhold approximately $4 billion in November benefits. Federal District Judge John McConnell of Rhode Island had ordered the government to release full funding using contingency reserves. Justice Ketanji Brown Jackson’s stay paused this order, allowing the 1st Circuit Court of Appeals additional time to review the case.

SNAP Program Facts (November 2025)

The legal dispute: The Trump administration argued that without new Congressional appropriations, the Executive Branch must prioritize available resources. The Department of Justice stated: “The core power of Congress is that of the purse, while the Executive is tasked with allocating limited resources across competing priorities.”

Judge McConnell countered that over $23 billion in contingency funds remained available within the child nutrition program, funded by tariff revenues, which could address the shortfall. Many recipients responded by seeking assistance from food banks or reducing essential expenditures, including medication purchases. Related coverage: Trump administration personnel and policy changes.

Housing Market Stress Signals

Multiple indicators confirm acute housing market stress extending beyond mortgage rates and affordability metrics:

The “lock-in effect” prevents many prospective sellers from listing homes because they retain ultra-low rates secured before borrowing costs increased in 2022. This supply constraint persists even as demand softens, keeping home prices elevated. See Fed policy signals on interest rate outlook.

Official Sources & Further Information

For detailed information on housing policy, mortgage assistance, and SNAP programs, refer to these authoritative resources from federal agencies:

What This Means

The Trump administration’s 50-year mortgage proposal and the Supreme Court’s SNAP funding stay represent two distinct policy responses to overlapping crises: housing affordability and food assistance access. Both involve complex tradeoffs between short-term relief and long-term consequences.

The 50-year mortgage reduces monthly payments but substantially increases total interest costs and extends debt obligations into buyers’ later years. Implementation would require coordination between the Federal Housing Finance Agency, congressional action to modify federal lending caps, and approval from Fannie Mae and Freddie Mac. No timeline has been provided. Related context: Bill Pulte’s role overseeing Fannie and Freddie.

The SNAP dispute remains an open legal question. The 1st Circuit Court of Appeals must decide whether the Supreme Court’s administrative stay should become permanent or whether the lower court’s full funding order will prevail. This determination will affect whether 42 million low-income Americans receive full benefits or face continued delays.

Both situations reflect the ongoing tension between immediate affordability relief and sustainable long-term policy solutions. Whether longer-term mortgages, interest rate adjustments, increased housing supply, or other interventions prove more effective will shape American homeownership and food security for years ahead.